Study Projects Louisiana Pension Funds to Run Dry in 2017

Louisiana’s largest pension program dismisses claims as “misleading”

NEW ORLEANS, La. – A Northwestern University study on state pension funds anticipates that by 2017 Louisiana will become fiscally insolvent, the second state to do so as a result of unfunded liabilities. The study contends that a “day of reckoning” is approaching, when state pension funds run out of money and states will either have to divert general revenues to cover retiree liabilities or default.

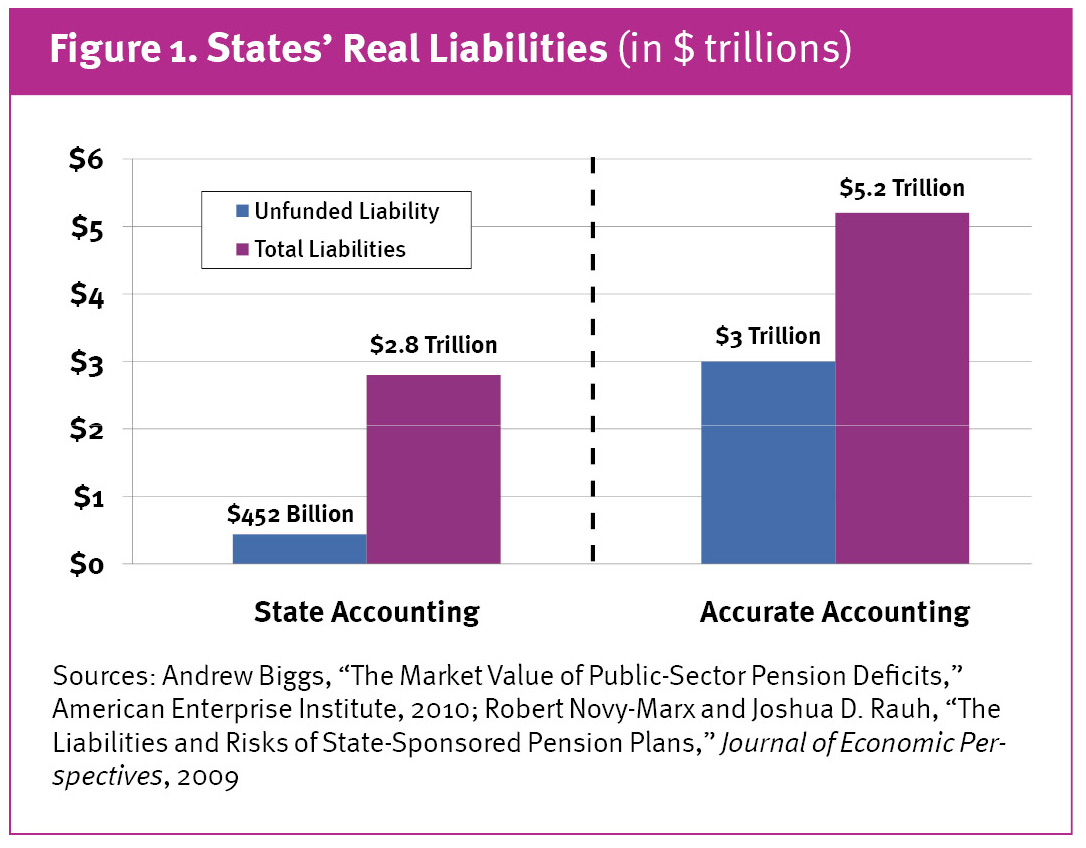

According to the study, “The Day of Reckoning for State Pension Plans,” state pension funds have total unfunded liabilities of $5.17 trillion, while states have set aside only $1.94 trillion. These dangerously unfunded pension plans will place “a substantial burden on state and local public finances in the near future,” says author and Northwestern professor Joshua Rauh.

He notes that pension funds have become more vulnerable in the last few years as a result of the downturn in the real estate and equities markets, along with longer life expectancies. Rauh projects that Oklahoma will be the first state to become insolvent as a result of unfunded pension liabilities, with Louisiana second in line.

He notes that pension funds have become more vulnerable in the last few years as a result of the downturn in the real estate and equities markets, along with longer life expectancies. Rauh projects that Oklahoma will be the first state to become insolvent as a result of unfunded pension liabilities, with Louisiana second in line.

As of 2008, Louisiana had unfunded liabilities of $11.7 billion, with total liabilities equal to $38.3 billion. And the latest, post-recession unfunded liability estimate is around $18 billion. Non-pension benefits such as retiree health care plans raise unfunded liabilities even further. If Louisiana pension funds run dry in 2017, the budget gap in 2018 would be $4.3 billion, or 28 percent of general tax revenue.

Louisiana policy makers have responded by closing loopholes in the pension system. In 2010, Governor Jindal signed into law HB519 to limit the Deferred Retirement Option Plan, which had previously allowed state employees to accrue pension payments for up to three years while remaining on public payrolls.

Additionally, the Louisiana legislature has mandated increased employee contribution percentages for the School Employees Retirement System, Louisiana State Employees Retirement System, the Judges Retirement Plan, and the State Police Pension Fund.

Keith Brainard, director of research for the National Association of State Retirement Administrators, disputes the study’s presentation of data. He argues that the amount needed to pay retirees is not the same as the state’s contribution to the pension fund, although presumably it would be if the fund ran dry and payments continued on.

“State and local spending on public pensions is the employers’ annual contribution to the pension trust – not the amount paid out of the trust each year to retirees,” said Mr. Brainard.

Brainard also seems to assume that current employees will continue to pay in, so as to maintain payments going out, highlighting the fragile nature of the pension system.

Louisiana State Employees’ Retirement Systems (LASERS), which represents 150,000 Louisiana residents and $8.9 billion in assets, also dismisses the study. Cindy Rogeou, executive director of LASERS, asserts that the pension program only accounts for 2.2 percent of Louisiana’s fiscal year 2010-2011 budget, and it led into the Great Recession with a 26 year compounded average actuarial return at 8.17%.

Rogeau believes Professor Rauh’s arguments are “misleading” and “create unwarranted alarm among the public”. She continues, “This type of academic analysis is not a true reflection of public pension solvency or actuarial soundness.”

Points of contention between LASERS and Northwestern’s report include Rauh’s assumptions that pension programs will only pay the normal costs of accruing benefits and not make payments into their Unfunded Accrued Liability account, discounting future pension liabilities at a risk-free rate rather than at expected returns of 8.25 percent, and that LASERS has had investment returns that exceeded expectations.

Robert Ross is a researcher and social media strategist with the Pelican Institute for Public Policy. He can be contacted at rross@pelicanpolicy.org, and you can follow him on twitter.